How to Help Escrow with Loan Packaging

IMPORTANT: Loan Packaging is work that is typically conducted by an escrow company. We are not an authority and cannot speak for any escrow, bank, or state’s guidelines. This is article is meant to give an idea concerning how loan packaging generally works. Consult each receiving agency’s specific guidelines.

What’s the purpose of loan packaging?

There are a lot of different parties involved in a loan transaction. When the final closing

documents arrive to the borrower via the notary, there are documents enclosed bound for

different destinations. The three parties most involved in the final steps of the loan closing are

the lender, the escrow, and the title company. So when the signed copies of the docs come back,

the escrow company will ‘package the loan a documents’ or prepare to send the different

documents to the parties that need them. The bank will want to retain the original signed copies

of their documents, the title company will need original copies of the deeds to be recorded, the

escrow company will want the original copies of their contract amendments. But that’s not all,

each of these agencies may also need copies of the other agencies paperwork to retain or utilize

for the completion of the transaction.

Packaging is typically the job of the escrow company, being able to help out on their behalf may

give you the edge when scoring a new company to work for.

Understanding why they package loan Documents

Each agency (lender, escrow, title) needs certain important documents to process or retain for

their protection in the loan process. ‘Loan document packaging’ is an industry term for

organizing the closing paperwork so that it is ready to send off to its appropriate agency. We’ll

describe the process, but first let’s envision the scenario.

Imagine holding the paperwork that the borrowers just signed. You’re in the escrow office and they have requested that you ‘package the loan documents’. They provide you with an empty desk and a nearby photo copier. That stack of loan documents that was just signed is about to triple in size. Your job is now to extract certain original documents from the pile of papers, make copies of them, and distribute them into 3 different piles. The first pile is for the escrow company, then a pile for the lender, then a stack for the title company. By the end of the process, each of the piles will have some blue ink signed original, and some photocopies.

Before we begin, can you contemplate who might need what originals and why? For Instance, what does the title company do? Which important document would they need an original of? What is the banks ultimate goal in lending money? which document might they want to retain to make sure this goal happens?

Imagine holding the paperwork that the borrowers just signed. You’re in the escrow office and they have requested that you ‘package the loan documents’. They provide you with an empty desk and a nearby photo copier. That stack of loan documents that was just signed is about to triple in size. Your job is now to extract certain original documents from the pile of papers, make copies of them, and distribute them into 3 different piles. The first pile is for the escrow company, then a pile for the lender, then a stack for the title company. By the end of the process, each of the piles will have some blue ink signed original, and some photocopies.

Before we begin, can you contemplate who might need what originals and why? For Instance, what does the title company do? Which important document would they need an original of? What is the banks ultimate goal in lending money? which document might they want to retain to make sure this goal happens?

1. Understand what the role of the institution in the lending process

- Lender

- Escrow

- Title

The escrow company is the neutral party that holds the money or property in trust and distributes when the conditions of the contract are met.

The title company can serve in many roles. They provide insurance to the bank and the buyer, protecting them from forgery, fraud, and liens. They also record documents (like deeds and riders) with the county.

2. Understand primary documents within a loan package

- Note (“IOU”)

- Deed of Trust (“Security Agreement” or “Lien Doc”)

- Grant Deed

- Riders

- Lending Instructions

- Escrow Contract Amendments

- Closing Disclosure (CD)

The Deed of Trust is the security instrument, it places a lien on the home to protects the bank. It gets recorded with the county. It protects the bank from a borrower running off with a large sum of money without consequence. If a borrower doesn’t pay the loan back or take care of home responsibilities like paying taxes, the bank may exercise on it’s right to foreclose on the home.

The Riders are most often addendum to the deed of trust (or note) to indicate a variation or update within the general terms of the document it is attached to. For example, a deed if trust may have a Planned Unit Development Rider (PUD) to show that the home falls within a homeowner’s association and is subject to its rules. The deed of trust riders are attached and recorded with the deed of trust.

The Grant Deed is the document signed by the seller to grant over the home to the new buyer. This document is held by the escrow company until the home is paid for according to the terms of the contract. It is recorded with county.

The Lending Instructions/Conditions are loan document instructions for the drafting and processing of a successful loan transaction. These instructions include conditions from homeowner’s insurance, to paying off credit cards, to the need for exact signatures on the loan documents. These instructions help everyone in the process carry out the terms of the lender.

Escrow Contract Agreements or Addendum are often found within atop the closing documents to satisfy the escrow’s contractual paperwork, transactional details between parties, and disclosure.

The Closing Disclosure is a government instituted mandatory form that provides full disclosure of the costs, loan, rate, and terms within a loan transaction. It is provided continually throughout the process to provide full disclosure to the borrowers of loan terms in an easily identifiable way.

3. Appropriate original signed documents received to each agency for closing

Remember, within that stack of 80-200 loan pages, there are a whole lot of separate documents. We

are going to pull some of the more important documents out and ultimately reorganize them all.

The bank, lender, and title company will want to retain any agreements and disclosure that pertain

to them or their responsibilities. The lender will want to retain an original copy of the Note, the

signed lending instructions, and leftover loan docs. The Escrow will want to retain their escrow

contract and addendum. The title company will need the original grant deed, deed of trust, and

riders for recording.

4. How to Package Loan Documents (3 stacks)

Create 3 spaces for the distribution of the piles of paper. The first pile will receive the documents

that escrow needs. The second pile will receive the documents that the lender receives. The third

pile will receive the documents that the title company needs.

First, will make copies of the crucial documents. Once these copies are made do not confuse them

with the originals. This is the primary reason we sign with blue ink, so that we can quickly identify

an original after copies are made.

Total Copies that are made as follows:

Total Copies that are made as follows:

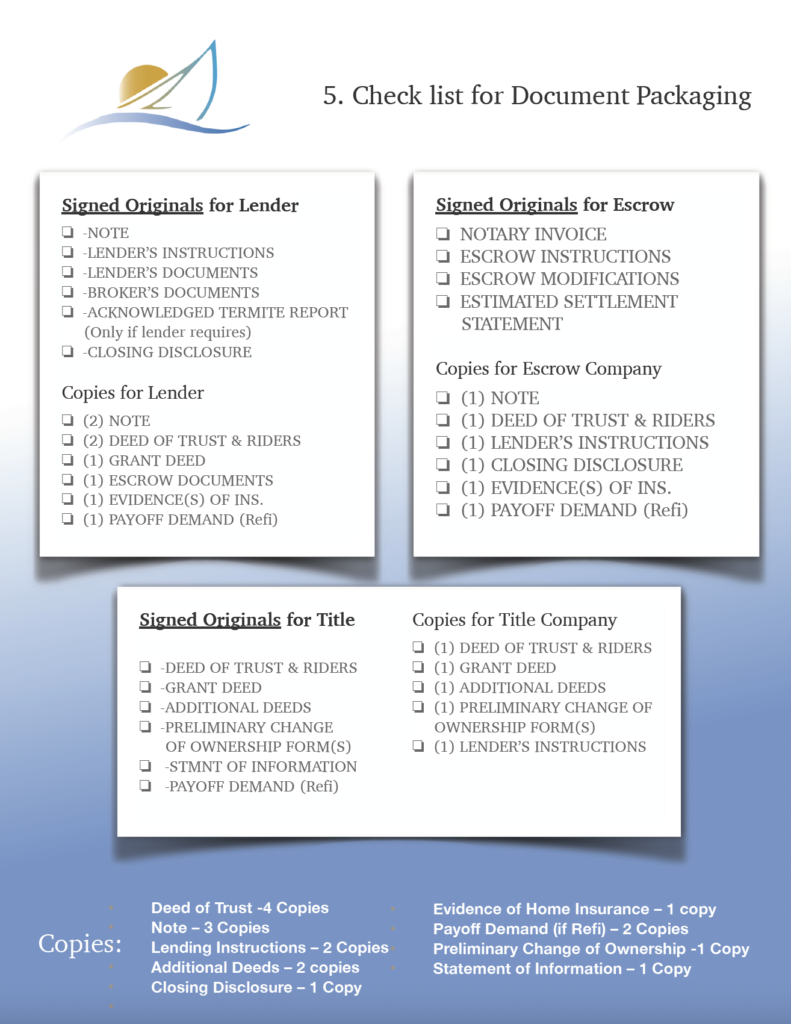

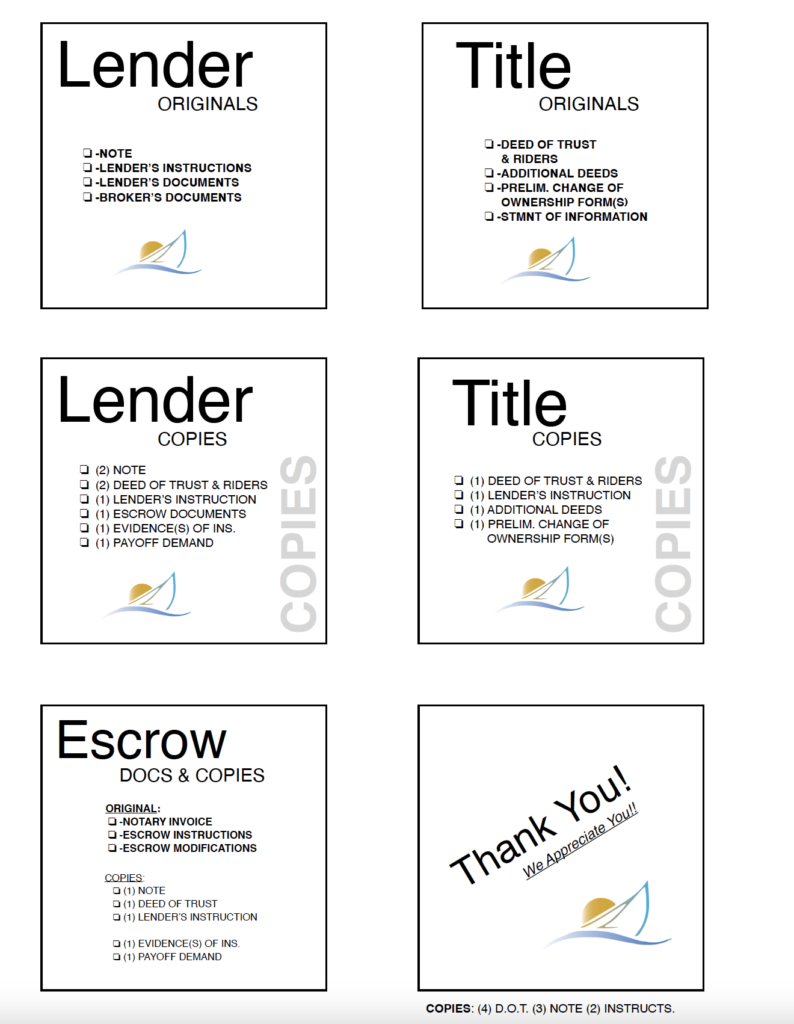

- Deed of Trust -4 Copies

- Note – 3 Copies

- Lending Instructions – 2 Copies

- Additional Deeds – 2 copies

- Closing Disclosure – 1 Copy

- Evidence of Home Insurance – 1 copy

- Payoff Demand to current loan (if a refinance) – 2 Copies

- Preliminary Change of Ownership Form -1 Copy

- Statement of Information – 1 Copy

5. Organization checklist for document packaging

Always reaffirm packaging procedures with your escrow officer first. There may be updates along the way. Consider these helpful checklists and organizational tools. IMPORTANT: Be mindful to keep original blue ink copies safe, unaltered, and untouched. Be careful escrow officers know the originals from copies. This is important because their”True and original copy” stamps only go on the duplicate black and white copies from the copier.

© SD Signings 2021 | Notary for Corporate Business, Law firms, and all of San Diego County | La Mesa | Mission Valley